No Interest Furniture Financing in Columbus 2026

A homeowner walks through a showroom, runs a hand across a solid-maple dining table, sits into a deep leather sectional, and immediately knows the piece belongs in the house. Then the practical question arrives. Is it wiser to wait, compromise, or find a payment structure that preserves cash for the rest of the project?

That moment is common in a full-home refresh. A move, renovation, growing family, or long-postponed upgrade often brings several decisions at once. Flooring, lighting, paint, window treatments, and furniture all compete for the same budget, even when the right furniture is meant to last far longer than many of the surrounding finishes.

No interest furniture financing can help bridge that gap. Used carefully, it isn't merely a retail perk. It's a planning tool that lets a household acquire lasting, bench-made furniture now while keeping the rest of the home budget intact. That matters most when the purchase is intended to serve for years, not seasons.

For homeowners thinking through the visual impact of a room before committing, resources on expert furnishings to make impressions can also help clarify how furniture shapes the experience of a space. Pairing that design perspective with a practical buying framework, such as this guide to shopping for furniture smartly, makes the financing conversation far less intimidating.

Table of Contents

- Investing in Your Home without the Upfront Cost

- The Two Types of No Interest Financing

- How Promotional Furniture Financing Plans Work

- What to Watch For to Avoid Costly Surprises

- Financing Your Custom Furniture at Vinson

- Smart Alternatives to Store Financing

- Frequently Asked Questions About Furniture Financing

Investing in Your Home without the Upfront Cost

A well-furnished home rarely comes together by accident. It comes from a series of deliberate choices about scale, comfort, craftsmanship, and longevity. That is especially true when a household is selecting solid cherry, oak, maple, or walnut furniture meant to anchor daily life for years.

In that setting, financing changes meaning. It stops being a way to "make do" and becomes a way to buy the right piece at the right time. A family replacing a temporary dining set with an Amish-made table and chairs isn't just adding furniture. They're choosing where holidays happen, where homework gets done, and where the home gathers its history.

Why the timing matters

Many furniture purchases happen alongside bigger transitions. A home closing date may be approaching. A renovation may be nearly complete. Guests may be arriving before custom pieces can be paid for entirely in cash without straining reserves.

A strong financing plan should support the home project, not compete with it.

That is where no interest furniture financing earns its place. It allows a homeowner to keep liquidity available for the rest of the move or remodel while still choosing durable pieces with substance, weight, and staying power.

Investment thinking changes the conversation

There is a meaningful difference between financing a disposable item and financing furniture built to age well. A bench-made dining set in solid hardwood, or a top-grain leather sectional with custom-fit comfort and refined motion features, serves a home differently than a short-term substitute.

That distinction matters because the homeowner isn't only comparing price tags. The actual comparison is often between:

- Buying once with intention and living with the result for the long run

- Buying twice through compromise after the first purchase fails to satisfy

- Delaying too long and continuing to live around temporary pieces that never quite fit the room

No interest furniture financing can make the first option possible without forcing a rushed cash decision. For a thoughtful homeowner, that isn't indulgence. It's disciplined planning.

The Two Types of No Interest Financing

The phrase "no interest" sounds simple, but shoppers often see two very different structures under that label. Knowing which one appears in the paperwork changes the entire risk level of the purchase.

One offer is simple and one can be risky

The safer version is commonly called true 0% APR. During the promotional period, the balance carries no interest, and the borrower pays the purchase down according to the stated schedule. If the plan is followed, the cost stays predictable.

The more complicated version is commonly called deferred interest. This arrangement often generates confusion. The offer may look harmless on the showroom tag, but the contract can work very differently if the full balance isn't paid by the deadline.

A useful way to think about it is this:

| Offer type | How it feels at checkout | What matters later |

|---|---|---|

| True 0% APR | A clear bridge from purchase to payoff | The borrower follows the schedule and avoids late issues |

| Deferred interest | A bridge that looks open | Missing the full payoff target can trigger costly consequences |

With deferred interest, the hidden problem isn't usually the monthly payment itself. It's the possibility that the promotion only stays harmless if every condition is met exactly.

Practical rule: If the financing language feels harder to explain than the furniture construction, the shopper should slow down and ask for the terms in plain English.

How to tell which one is in front of you

The contract usually gives clues. The safest approach is to read beyond the bold headline and focus on the sentences that describe what happens at the end of the promotional window.

Shoppers should look for wording around:

- Paid in full requirement. If the balance must be fully cleared by a specific date to avoid charges, the plan may be deferred interest.

- Equal monthly payments. This language often signals a structured payoff path, but it still needs verification.

- Late payment consequences. A single late payment can change the economics of the offer.

- Regular APR after the promotion. Even if the promotional period is attractive, the ongoing account terms still matter.

A quick review of current furniture promotions and financing offers can help a shopper see how retailers present these structures, but the contract language always matters more than the headline graphic.

A better question than "Is it no interest"

Many buyers ask whether financing is available. The more useful question is whether the financing is forgiving or fragile.

A forgiving plan gives the homeowner room to execute the payoff with confidence. A fragile plan works only if timing, payment allocation, and account handling all go exactly right. Furniture should make a home feel settled. The financing shouldn't introduce uncertainty that follows the buyer home.

How Promotional Furniture Financing Plans Work

Most promotional furniture financing plans are built around one central idea. A large purchase gets divided into manageable monthly payments over a set promotional term. That structure can be very useful for custom furniture, full-room projects, or a coordinated replacement of several worn pieces at once.

The payment structure is usually the main feature

Industry explainers note that promotional periods commonly run from 3 to 60 months, with many furniture retailers using 6, 12, 24, 36, or 48 months of 0% APR financing. One clear example from a furniture financing explainer shows that a $3,000 purchase divided across 36 months comes to about $83.34 per month, which illustrates why these offers are often framed as a budgeting tool for larger purchases (payment example and promotional period reference).

That math matters because it turns a vague idea into a practical decision. A homeowner can compare the monthly obligation against the rest of the home budget and ask whether the schedule fits comfortably, not just technically.

Approval usually depends on preparation

Approval standards vary, but lenders typically want evidence that the borrower can handle the account responsibly. That usually means the shopper should review credit standing, verify income details, and avoid applying casually without understanding the terms.

A simple preparation process often helps:

- Check current credit information before entering the showroom.

- Review the household budget and decide what monthly amount feels sustainable.

- Know the full purchase scope. A dining set, bedroom suite, and motion seating may be financed differently than a single item.

- Ask how custom orders affect timing so the payment plan aligns with delivery expectations.

The cleanest financing experiences usually happen when the room plan and the payment plan are built together.

For buyers considering solid wood furniture in Ohio, Amish-made dining sets, or custom leather sectionals in Columbus, this preparation keeps the purchase grounded. It becomes less about whether financing is available and more about whether the structure matches the household's actual priorities.

Why financing can work well for larger furniture decisions

Furniture often functions as a group purchase, not a single-item transaction. A room may need a table, host chairs, side chairs, and storage. A living room may need a sectional, swivel chair, and recliner. Promotional financing can help those coordinated decisions happen in one coherent phase instead of over several disconnected purchases.

Shoppers who want to review available furniture financing options should still start with the same question. Can the promotional term comfortably retire the balance before any less favorable terms begin? If the answer is yes, financing can be a disciplined way to complete a room with consistency and intention.

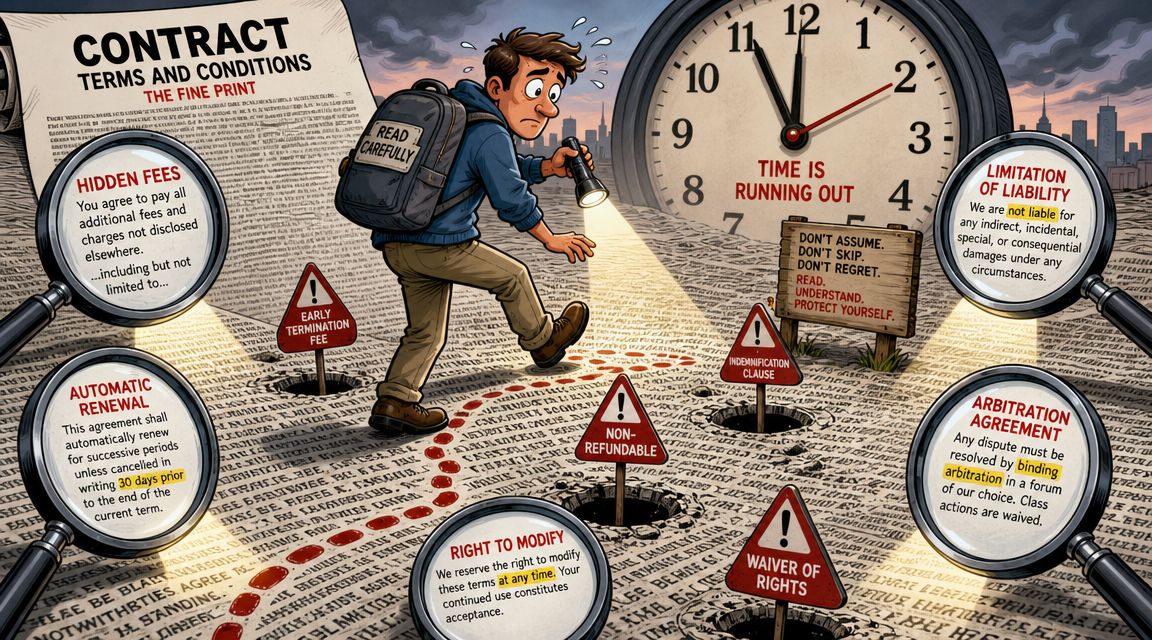

What to Watch For to Avoid Costly Surprises

Promotional financing works best when the shopper treats the agreement with the same care used to evaluate wood species, leather grade, or joinery. The danger isn't usually the visible monthly payment. The danger is the clause that only becomes important after the papers are signed.

Fine print matters more than the headline

Many consumer guides gloss over what happens after the promotion ends. One current major-retailer example lists a 34.99% purchase APR and 39.99% penalty APR for new accounts, which shows how expensive a missed payoff or account issue can become (current APR and penalty APR example).

That single fact changes how a prudent buyer should read every offer. The attractive part of the promotion is only one layer. The backup terms matter just as much, because they determine the cost of a mistake.

A shopper doesn't need to become a credit expert. A shopper does need to become careful.

A short checklist before signing

The most important protection is a deliberate read-through of the account terms. These are the places where costly surprises tend to hide:

- Promotional payoff deadline. Verify the exact date by which the full promotional balance must be cleared.

- Late payment treatment. Ask what happens if a payment posts late, even once.

- Minimum payment language. Minimums may keep the account current without retiring the promotional balance in time.

- Purchase thresholds. Some offers only apply if the transaction reaches a required amount.

- Equal payment structure. Confirm whether the schedule is designed to fully pay off the balance within the promotional term.

- Post-promotion APR. Even if the household expects to pay in time, the backup rate should still be understood before signing.

A financing offer is only as attractive as its worst-case terms.

That doesn't mean these programs should be avoided. It means they should be used with precision. A homeowner who sets reminders, pays ahead when possible, and tracks the promotional end date can often avoid the most common problems entirely.

Good habits lower the risk

Furniture financing becomes safer when the borrower builds a simple management system around it. That can include automatic payments, a calendar reminder before the promotional period ends, and a written payoff target rather than relying on the minimum shown on the statement.

A return, exchange, or delivery delay can also affect the account balance and schedule. Reviewing the retailer's store policies for orders, returns, and related details helps the buyer understand how logistics and financing may interact.

For larger home purchases, clarity is calming. The household should know not only what it is buying, but exactly how the purchase will be paid off and what could disrupt that plan.

Financing Your Custom Furniture at Vinson

Financing becomes especially useful when the goal isn't to grab something close enough, but to order the exact piece the room needs. That is often the case with solid-wood dining furniture, coordinated bedroom collections, and customized seating where scale, finish, leather, and motion options all matter.

Financing can protect the design vision

A custom order often asks a homeowner to think beyond the immediate transaction. The family isn't selecting from whatever happens to be on a floor. They're choosing dimensions, silhouettes, fabrics, finishes, and details that allow the furniture to live properly in the home.

That can make financing more strategic. Instead of settling for a piece that is available today but wrong in tone, depth, or finish, the homeowner can preserve the design plan and spread the cost across a manageable schedule.

This is where custom furniture ordering options matter. A Custom Order Program with fabrics, finishes, and visualizers helps buyers shape a room around their actual home rather than around a compromise.

Where value and planning meet

Vinson Fine Furniture offers financing through the Synchrony HOME Credit Card, and that can be useful for qualified buyers who want to pair design decisions with a structured payment path. In practice, that may help a household move forward on a Smith Brothers sectional in top-grain leather, a Canadel dining configuration, or a Mavin bedroom suite in solid cherry, oak, maple, or walnut without abandoning the broader renovation budget.

Several core benefits become more relevant when financing and design are considered together:

- Customization support. Custom Order options make it easier to choose the right fabric, finish, or configuration rather than the nearest substitute.

- Design services. An in-store design studio and complimentary consultations help align the purchase with the room's scale, traffic flow, and visual balance.

- Quality focus. Solid hardwood construction and premium motion seating options support the logic of investing in furniture intended to last.

- Value protections. A low price guarantee and a clearance gallery can help buyers compare whether financing the full custom vision or selecting immediate savings better suits the household plan.

For some homeowners, the best use of financing may be a whole-room project. For others, it may be the one anchor piece that changes how the entire home feels. A custom leather sectional with smooth power motion, a set of Amish-made dining chairs built around the table's exact finish, or a fully matched bedroom suite often carries more long-term satisfaction than a patchwork approach.

Furniture planning works best when comfort, construction, and cash flow are considered at the same time.

That is why the showroom experience still matters. Sitting in a swivel chair, testing the glide of a rocker, comparing wood tones in person, and feeling the hand of leather are all part of deciding whether the financed purchase is worthy of the commitment.

Smart Alternatives to Store Financing

Store financing isn't the only responsible route. Sometimes another payment strategy fits the household better, especially if the buyer wants all borrowing in one place or prefers terms from an existing banking relationship.

When another route may fit better

A few alternatives can make sense depending on the situation:

| Option | Often useful when | Main consideration |

|---|---|---|

| Personal loan | The buyer wants a fixed structure through a bank or credit union | The interest cost may be more predictable, but not always lower |

| Introductory APR credit card | The buyer is highly organized and confident about payoff timing | The promotional window still needs careful tracking |

| Cash savings approach | The room can wait and the household wants zero financing complexity | Delay may postpone the design outcome |

| Combination strategy | Part of the project is financed and part is paid directly | Requires careful budgeting across multiple sources |

Some buyers also prefer flexible payment models in other furnishing contexts. For example, teams evaluating nontraditional arrangements can review Flexible workspace furniture plans to understand how payment structure can vary by use case, even though a long-term residential purchase usually calls for a different standard of durability and ownership.

The strongest choice is the one that fits the purchase and the household's habits. If a buyer is meticulous about due dates, store financing may work well. If simplicity matters more than a promotional headline, a conventional loan may feel easier to manage. The furniture should fit the room. The payment method should fit the person.

Frequently Asked Questions About Furniture Financing

Common questions that come up at the end

How does applying for furniture financing affect a credit score?

Applying often involves a credit inquiry. That can affect a score, and the impact depends on the lender's process and the buyer's broader credit profile. The practical takeaway is simple. A shopper should apply thoughtfully, not casually at multiple places in a short span.

Can promotional financing be used on clearance furniture?

That depends on the retailer's specific program and the terms attached to the sale item. Some households find that clearance savings make financing unnecessary, while others use financing to complete a room efficiently even when they are buying value-oriented pieces. The important step is to verify eligibility before checkout rather than assume every item qualifies the same way.

What happens if a financed item is returned?

Returns and exchanges can change the account balance, the promotional structure, or both. A buyer should ask how credits are applied and whether the promotional term changes after a return. That question matters most on custom orders and multi-item purchases where one adjustment can affect the whole transaction.

Is no interest furniture financing a good idea for custom furniture?

It can be, especially when the buyer is using it to avoid compromising on material, scale, or finish. The key is that the payment plan should match the pace of the household budget and the expected timeline for the project.

Should a buyer finance a single statement piece or a whole room?

Either approach can work. The better answer usually depends on whether the room needs cohesion immediately or whether one anchor piece can carry the design forward while the rest of the space evolves.

A thoughtful home deserves thoughtful buying decisions. Homeowners exploring solid wood furniture in Ohio, Amish-made dining sets, custom leather sectionals in Columbus, or custom-designed bedroom and motion seating can review options and plan a visit through Vinson Fine Furniture. The Easton Town Center showroom offers a chance to test comfort, compare finishes, discuss custom possibilities, and evaluate whether a financing plan fits the project with clarity.